ESG Investing: Financing Renewable Energy via Sustainable Markets

July 8, 2019

By Max Almono

On June 17, ACORE hosted an Executive Meeting in New York City to examine how Environmental, Social, and Governance (ESG) disclosure and scoring methodologies can better reflect renewable energy use and investment. Participants at the event included leading investors, utilities, corporate offtakers, credit rating agencies, and professional service firms.

Speakers from BlackRock, CDP, CleanCapital and Pillsbury Winthrop Shaw Pittman LLP started us off with a panel on how institutional investors are leveraging ESG methodologies to develop climate-friendly funds. The second panel featured experts from Citi, Ingersoll Rand, IBM, and S&P Global (Trucost) addressing how improved ESG disclosure practices and scoring methodologies can increase demand for renewable energy. This blog details key takeaways from these discussions.

ESG Market Lacks a Universal Taxonomy

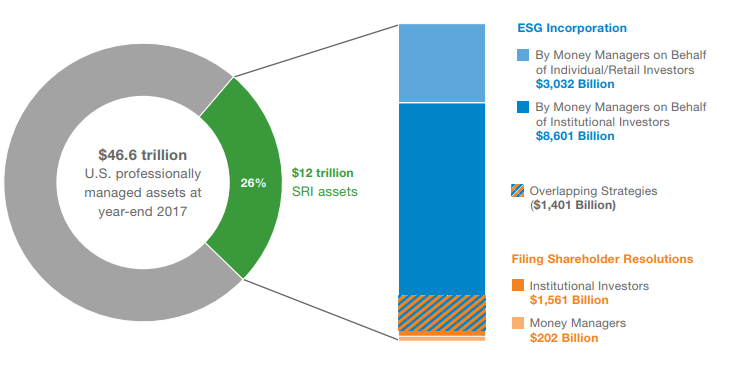

Demand for ESG investment has increased exponentially over the last few years. Sustainable, responsible, and impact (SRI) investing now totals close to $12 trillion in U.S. assets under management (Figure 1). Of that, nearly a fourth is being used to help combat climate change. However, despite popular demand and growing pressure from industry stakeholders, the ESG community lacks a standard taxonomy. Panelists and attendees agreed that there is an urgent need to converge disparate ESG methodologies.

A standardized reporting framework would alleviate the burden on companies seeking to improve their scores by distilling comparable metrics. The Task Force on Climate-related Financial Disclosures (TCFD) is one framework that could function as a baseline for industry stakeholders on climate. TCFD was established by the Financial Stability Board in 2015 with a remit to develop recommendations for companies to disclose their climate-related financial risks. Global initiatives like the Better Alignment Project seek to unify the Climate Disclosure Standards Board (CDSB), the Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC) and the Sustainability Accounting Standards Board under the TCFD recommendations.

Leading ESG data aggregators, like CDP (formerly the Carbon Disclosure Project), are also aligning with the TCFD. In June 2019, CDP released a report highlighting that the 215 largest global companies have almost $1 trillion at risk from potential climate impacts. Conversely, the report estimates that the business opportunity could reach nearly $2.1 trillion if companies decide to act on climate change. This analysis helped illuminate significant macroeconomic risks and challenges through the lens of the TCFD recommendations.

Institutional Investors Want Material Information

The quality of ESG data has come under scrutiny as institutional investors look to establish climate resilient funds. According to the Harvard Business School, on average, roughly 20% of ESG data is considered material (i.e., indicative of financial performance) to investors. This low figure is primarily due to transparency issues, inconsistent reporting metrics, and “black box” calculations. Most corporations use boilerplate language and check-the-box answers, which supplant more relevant ESG performance-use indicators such as energy intensity and GHG emissions. Therefore, it comes as no surprise that most investors are dissatisfied with the quality of ESG data. Many studies have shown how the use of proprietary calculations have often led to arbitrary scores.

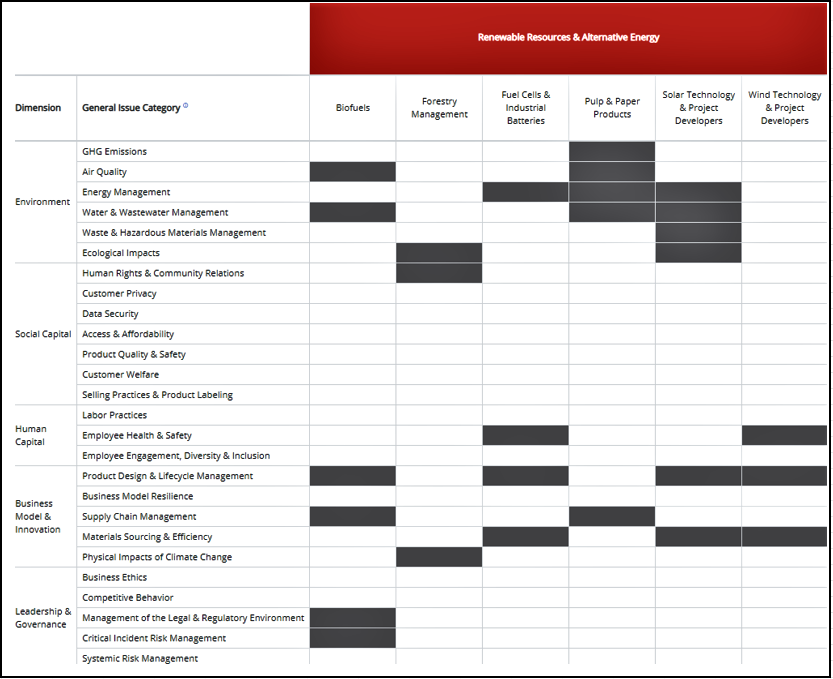

Organizations like the Sustainability Accounting Standards Board (SASB), help cut through superfluous ESG information by placing a strong emphasis on sector-specific material-use indicators. As seen in Figure 2, SASB created a materiality map which identifies the most relevant ESG metrics for the renewable energy industry.

During the event, panelists reiterated the need for material information at both the portfolio and asset levels. In order to establish relevant ESG analysis, renewable energy developers and lenders need to adopt transparent and consistent reporting metrics. These metrics will help institutional investors better understand the correlation between ESG disclosure and portfolio returns.

The Relationship Between ESG Investing and Renewable Energy Is Still Evolving

In the context of ESG disclosure, the renewable energy industry can be grouped into four different constituencies: Institutional Investors, Capital & Service Providers, Power Generation and Renewable Offtakers. The alignment of all four constituencies can help strengthen the relationship between ESG investing and renewable energy deployment.

During the Executive Meeting, speakers highlighted the need for stronger metrics around avoided carbon emissions. Under current GHG accounting principles, capital and service providers are only allowed to claim partial credit for the avoided emissions of their downstream investment activities. The absence of an avoided emissions credit has subsequently undervalued climate-friendly lenders and companies. Panelists also discussed approaches to expand the robustness of Scope 2 emissions, which the Greenhouse Gas Protocol defines as all indirect emissions from the generation of purchased energy. In the context of ESG reporting, the material differences between VPPAs, RECs, location of purchase, and time-of-use are often not fully disclosed. If investors care about GHG reductions, corporate Scope 2 reporting should reveal how renewable energy procurement is directly reducing carbon emissions.

In January 2019, ACORE launched an ESG working group comprised of institutional investors, lenders, corporate offtakers, and utilities. The working group seeks to increase demand for renewable energy by ensuring ESG scoring methodologies more accurately reflect the full value of companies’ renewable energy use and investment. ACORE will use the feedback provided by Executive Meeting participants to inform the development of recommendations for best practices in ESG investing.

Join leaders from across the clean energy sector.

What will our next 20 years look like? Here’s the truth: they’ll be better with ACORE at the forefront of energy policy.

Shannon Kellogg

Amazon Web Services (AWS)